Two more US banks have just failed, bringing the total this year to 19:

The FDIC estimates that through 2013 there will be about $40 billion in losses to the deposit insurance fund, including an $8.9 billion loss from the failure of IndyMac Bank. The FDIC is raising insurance premiums paid by banks and thrifts to replenish its fund, which now stands at around $45.2 billion, below the minimum target level set by Congress and the lowest level since 2003.

The current target (the "Designated Reserve Ratio") is 1.25% of deposits and is discussed here. According to Mish on July 23, insured deposits in the US banking system totalled $4.24 trillion, which if unchanged now would mean the FDIC current funds represent 1.066% of the sum insured, s0 the FDIC needs to raise another c. $8 billion in premiums from banks.

The question remains, whether merely 1.25% is sufficient for present and foreseeable circumstances. Dr Marc Faber is now talking about eventual US inflation and State bankruptcy - after a near-term rally.

Showing posts with label depositor protection. Show all posts

Showing posts with label depositor protection. Show all posts

Sunday, November 09, 2008

Like I said

I've said more than once, including in my latest letter to the Spectator, the notion that the East is going to suffer from the slump as badly as the West needs some qualification. It's what happens after the slump that will be decisive, and the East has the gear and skilled people to lead the way out, as the Telegraph reports:

Arcelor, being three times larger than its nearest rival, Japan's Nippon Steel, and sharing 10 pc of the industry's global sales, wields huge power to determine what happens to prices and production. In the medium to longer term, Mr Mittal expects the industry to bounce back sharply as the pace of industrialisation in China and India picks up again.

In China, billionaire Shagang steel magnate Shen Wenrong has also planned for the coming downturn. In fact he's not even cutting his prices, since (I surmise) his game plan is that his over-leveraged competitors are going to go bust and customers will have to come to him anyway.

This is smart, counter-intuitive strategy for dealing with a recession. Those who try to survive by cutting margins will get skinny and become more vulnerable to delayed delivery by cash-strapped suppliers, bad-debt customers, and shark bigger-business customers that deliberately pay late to force your business under and then buy your goods from the official receiver at a 90% discount.

In a really post-industrial economy, we in the UK and USA will discover the disadvantages of being run by money-grows-on-trees lawyers, box-it-all-up-and-get-it-on-the-train-before-the-war-ends bankers and hang-onto-office-by-your-bitten-fingernails politicians.

My plan? Pay off debts, hoard some emergency cash (and maybe gold), and if I have to invest, put it in something that's secure and inflation-proofed.

Arcelor, being three times larger than its nearest rival, Japan's Nippon Steel, and sharing 10 pc of the industry's global sales, wields huge power to determine what happens to prices and production. In the medium to longer term, Mr Mittal expects the industry to bounce back sharply as the pace of industrialisation in China and India picks up again.

In China, billionaire Shagang steel magnate Shen Wenrong has also planned for the coming downturn. In fact he's not even cutting his prices, since (I surmise) his game plan is that his over-leveraged competitors are going to go bust and customers will have to come to him anyway.

This is smart, counter-intuitive strategy for dealing with a recession. Those who try to survive by cutting margins will get skinny and become more vulnerable to delayed delivery by cash-strapped suppliers, bad-debt customers, and shark bigger-business customers that deliberately pay late to force your business under and then buy your goods from the official receiver at a 90% discount.

In a really post-industrial economy, we in the UK and USA will discover the disadvantages of being run by money-grows-on-trees lawyers, box-it-all-up-and-get-it-on-the-train-before-the-war-ends bankers and hang-onto-office-by-your-bitten-fingernails politicians.

My plan? Pay off debts, hoard some emergency cash (and maybe gold), and if I have to invest, put it in something that's secure and inflation-proofed.

Sunday, October 05, 2008

How to force the UK Government to give 100% guarantee on your deposits

... Transfer all your money to National Savings and Investments.

Their guarantee:

"Backed by HM Treasury

100% secure

National Savings and Investments is backed by HM Treasury, so any money you invest with us is 100% secure."

The Easy Access Savings Account can take up to £2 million per person. In all, depending on your age, NS&I could take more than £6 million per head.

If enough people know about this, and act on it, only Northern Rock will be run-proof. HMG will have to provide an "Irish guarantee". Unless, of course, the Chancellor suddenly welches on government credit, and that really would be the end; or closes the door to new NS&I deposits.

Get in while you can?

But not into Ireland:

However, experts are already raising questions over the Irish scheme, and asking how much protection it really affords. Adrian Coles, the director general of the Building Societies Association, said savers should write to the Irish Embassy to ask them how they intended to guarantee UK savings, and how they would obtain enough sterling in the event of a bank failing.

However, experts are already raising questions over the Irish scheme, and asking how much protection it really affords. Adrian Coles, the director general of the Building Societies Association, said savers should write to the Irish Embassy to ask them how they intended to guarantee UK savings, and how they would obtain enough sterling in the event of a bank failing.

"Has the Irish government quantified the potentially huge liabilities it is taking on by guaranteeing sterling deposits in Britain, where household cash savings amount to £1.1 trillion?" he said.

"Savers should beware that, if they switch accounts to take up this guarantee, they are effectively betting on the Irish government's ability to buy sufficient sterling in the foreign exchange markets.

Their guarantee:

"Backed by HM Treasury

100% secure

National Savings and Investments is backed by HM Treasury, so any money you invest with us is 100% secure."

The Easy Access Savings Account can take up to £2 million per person. In all, depending on your age, NS&I could take more than £6 million per head.

If enough people know about this, and act on it, only Northern Rock will be run-proof. HMG will have to provide an "Irish guarantee". Unless, of course, the Chancellor suddenly welches on government credit, and that really would be the end; or closes the door to new NS&I deposits.

Total retail deposits in the UK are now around £1.17 trillion, of which nearly half is not covered even by the £50,000 deposit protection limit that came into force on October 3rd. So if everybody takes appropriate action, NS&I (and/or Northern Rock) should expect an influx of about £468 billion pounds.

Funds invested in NS&I stood at £84.8bn in 2007/08. A full-scale "flight to safety" would entail an abrupt 550% increase in their deposits.

Get in while you can?

But not into Ireland:

However, experts are already raising questions over the Irish scheme, and asking how much protection it really affords. Adrian Coles, the director general of the Building Societies Association, said savers should write to the Irish Embassy to ask them how they intended to guarantee UK savings, and how they would obtain enough sterling in the event of a bank failing.

However, experts are already raising questions over the Irish scheme, and asking how much protection it really affords. Adrian Coles, the director general of the Building Societies Association, said savers should write to the Irish Embassy to ask them how they intended to guarantee UK savings, and how they would obtain enough sterling in the event of a bank failing. "Has the Irish government quantified the potentially huge liabilities it is taking on by guaranteeing sterling deposits in Britain, where household cash savings amount to £1.1 trillion?" he said.

"Savers should beware that, if they switch accounts to take up this guarantee, they are effectively betting on the Irish government's ability to buy sufficient sterling in the foreign exchange markets.

Wednesday, September 17, 2008

Is the "cash" in your pension fund safe?

There's been much talk of keeping the balance in your bank account/s below the insured limit - but if you are cautious and want to preserve the value of what's in your pension pot, how can you do it?

"Mish" reports a massive write-off by a money market fund manager, following losses with Lehman.

UPDATE:

If you have funds in a money market and it is not backed by only Treasury debt, you need to consider moving that money right here, right now. - Karl Denninger

"Mish" reports a massive write-off by a money market fund manager, following losses with Lehman.

UPDATE:

If you have funds in a money market and it is not backed by only Treasury debt, you need to consider moving that money right here, right now. - Karl Denninger

Wednesday, July 23, 2008

Mish: "The entire US banking system is insolvent."

Mish gives us a long list of bad news; the last item is, arguably, the worst:

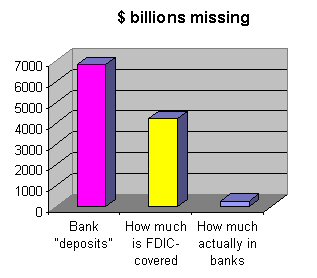

Of the $6.84 Trillion in bank deposits, the total cash on hand at banks is a mere $273.7 Billion. Where is the rest of the loot? The answer is in off balance sheet SIVs, imploding commercial real estate deals, Alt-A liar loans, Fannie Mae and Freddie Mac bonds, toggle bonds where debt is amazingly paid back with more debt, and all sorts of other silly (and arguably fraudulent) financial wizardry schemes that have bank and brokerage firms leveraged at 30-1 or more. Those loans cannot be paid back.

What cannot be paid back will be defaulted on. If you did not know it before, you do now. The entire US banking system is insolvent.

Tuesday, July 15, 2008

Bank deposits are investments, and can go wrong

Karl Denninger takes us back to basics about banks and "your money" (highlighting is mine):

I want to talk about IndyMac for a bit.

The news has covered a few really, truly sad stories. People with $200,000, $300,000, $400,000 or more in there who have seen 50% of their balance over $100k disappear overnight.

Older people who literally have their life savings in these institutions. People who are relatively unsophisticated, but have been told through the years that the government will make it all ok, and who believed it.

It tugs at your heart to see a 70+ year old man pleading for them to let him have his money - money that he worked and saved a lifetime for.

If only it were that easy.

People don't think of a bank as being an investment, but it is.

You are lending your money to the bank so they can make money with it, and they pay your a coupon - interest, or the "safekeeping" in the case of a checking account that does not pay interest - in return!

I want to talk about IndyMac for a bit.

The news has covered a few really, truly sad stories. People with $200,000, $300,000, $400,000 or more in there who have seen 50% of their balance over $100k disappear overnight.

Older people who literally have their life savings in these institutions. People who are relatively unsophisticated, but have been told through the years that the government will make it all ok, and who believed it.

It tugs at your heart to see a 70+ year old man pleading for them to let him have his money - money that he worked and saved a lifetime for.

If only it were that easy.

People don't think of a bank as being an investment, but it is.

You are lending your money to the bank so they can make money with it, and they pay your a coupon - interest, or the "safekeeping" in the case of a checking account that does not pay interest - in return!

US banks: uninsured deposits stand at $2.6 trillion

Mish calculates the potential for disaster if depositors lose confidence:

"FDIC Recap

There is $6.84 Trillion in bank deposits.

$2.60 Trillion of that is uninsured.

Total cash on hand at banks is $273.7 Billion."

So 89% of uninsured deposits are not covered by available cash in the bank.

"FDIC Recap

There is $6.84 Trillion in bank deposits.

$2.60 Trillion of that is uninsured.

Total cash on hand at banks is $273.7 Billion."

So 89% of uninsured deposits are not covered by available cash in the bank.

Wednesday, July 09, 2008

Saturday, May 17, 2008

Check your bank deposit security

A cautionary story from Michael Panzner here. An American nearly lost most/all of $400,000 deposited with his bank, despite taking great care to set up the account in a way that brought it under the FDIC deposit protection scheme.

An intriguing detail is the reluctance of the bank to let the account be titled appropriately - failure to do which could have cancelled the FDIC protection. Another, is the bank's reluctant and misleading response when the depositor tried to exercise his right to withdraw his cash.

And the $15,000 interest was lost, anyway.

Where is your account? Make sure it's not dead money.

Wednesday, April 16, 2008

Weaknesses in US depositor protection

A very timely article from Financial Sense on the FDIC and its limitations. After reading this, UK depositors may not be so keen to replicate the system.

htp: Michael Panzner's "Financial Armageddon" blog.

htp: Michael Panzner's "Financial Armageddon" blog.

Thursday, August 30, 2007

Money safety update - American banks

"I warn you, Sir! The discourtesy of this bank is beyond all limits. One word more and I—I withdraw my overdraft." (Punch, June 27, 1917)

"I warn you, Sir! The discourtesy of this bank is beyond all limits. One word more and I—I withdraw my overdraft." (Punch, June 27, 1917)I recently looked at the security of deposits in British banks, but what about the USA? As with my earlier post this morning, we find concise information included in a different argument, in this case about the American liquidity crisis.

In the USA, it seems that up to $100,000 in checking and savings accounts (per depositor per "member bank") is covered by the Federal Deposit Insurance Corporation. There were two separate funds - one for banking, the other for savings (following the $150 billion losses in the savings & loan crisis a generation ago) - but they have been merged as from the end of March 2006.

There are three compensation methods used. One is direct payment to the investor, termed a "straight deposit payoff". The other two involve transfer of business to a healthy bank, with some financing from FDIC: these are known as "purchase and assumption" (P&A) and "insured deposit transfer" - full details here and here. (N.B. although FDIC prefers not to make a straight deposit payoff, as it is the most expensive solution for them, it remains an option - Sutton and Hagmahani's brief account skates over this point.)

The $100k upper limit for depositor protection is more generous than in the UK - and it seems to be 100% insured, unlike for the poor British saver. But, the authors warn, FDIC "only works when bank failures are isolated events, and will not work in a systemic crisis...or for that matter one really big bank failure."

Taking a more general view, the article explains that the subprime mess has reduced liquidity in the system, causing it to work inefficiently, which is why the Federal Reserve has pumped in more cash - accepting "toxic waste" collateral in return, and offering a discount on its loan rate to banks.

The authors have two objections to this assistance:

- it rewards bad behaviour and encourages a repetition ("moral hazard")

- accepting unrealizable obligations as collateral is inflationary, since it turns nothingness into money

Their prediction: a fall in the value of the dollar, and if the banks disguise their problems and fail to clean house, at worst a collapse of the financial system. The Fed has bought some time, but that time has to be used for urgent reform.

Thursday, August 23, 2007

Is your money safe in the bank?

Mike Shedlock, in The Daily Reckoning Australia today, raises a point we should all consider - how far your cash deposits are protected by law. This is NOT an academic question - a hard-working and thrifty truck driver has recently lost over $300,000 of his life savings in the Metropolitan Savings Bank in Lawrenceville.

For British savers, here is the current position:

"Financial Services Compensation Scheme

The Financial Services Compensation Scheme (FSCS) was created and put into operation in December 2001. It was brought in to replace the Building Societies Investor Protection Scheme, Deposit Protection Scheme and several other schemes previously in place. The FSCS was introduced to protect customers of firms that go into liquidation or out of business.

The scheme is activated when an authorised firm goes out of business or the Financial Services Authority (FSA) considers that an authorised firm is unable or unlikely to be able to repay their customers.

Most customers are partially protected under this scheme and are entitled to the following amount of compensation:

The compensation limit applies to individuals and covers the total amount of all their deposits held with that firm. Each individual in a joint account is eligible to receive compensation up to the maximum limit in respect of his or her share of the deposit. The FSCS assumes the account is equal and splits it 50:50 unless evidence shows otherwise.”

Source: http://www.moneysupermarket.com/savings/GuideToSavings.asp (accessed 17 Aug 07)

From this you can see that for your savings lodged with any one deposit taker, any excess over £35,000 for a single account holder, or £70,000 for joint (50:50) holders, is not protected.

Some may say, "It can't happen here", but it did in the Isle of Man in 1982, where the Savings & Investment Bank collapsed, losing £42 million of depositors' money. International bank BCCI collapsed in 1991 with debts of £10 billion, hitting 6,500 British depositors - and the legal case against the bank ultimately collapsed as well.

Savings schemes are not safe, either. About £41 million was lost in the Farepak Christmas hamper collapse last year.

The strategy is to know your rights, and to diversify. As Antonio says in The Merchant of Venice:

My ventures are not in one bottom [i.e. ship's keel] trusted,

Nor to one place; nor is my whole estate

Upon the fortune of this present year:

Therefore my merchandise makes me not sad.

For British savers, here is the current position:

"Financial Services Compensation Scheme

The Financial Services Compensation Scheme (FSCS) was created and put into operation in December 2001. It was brought in to replace the Building Societies Investor Protection Scheme, Deposit Protection Scheme and several other schemes previously in place. The FSCS was introduced to protect customers of firms that go into liquidation or out of business.

The scheme is activated when an authorised firm goes out of business or the Financial Services Authority (FSA) considers that an authorised firm is unable or unlikely to be able to repay their customers.

Most customers are partially protected under this scheme and are entitled to the following amount of compensation:

100% of the first £2,000

90% of the next £33,000

The compensation limit applies to individuals and covers the total amount of all their deposits held with that firm. Each individual in a joint account is eligible to receive compensation up to the maximum limit in respect of his or her share of the deposit. The FSCS assumes the account is equal and splits it 50:50 unless evidence shows otherwise.”

Source: http://www.moneysupermarket.com/savings/GuideToSavings.asp (accessed 17 Aug 07)

From this you can see that for your savings lodged with any one deposit taker, any excess over £35,000 for a single account holder, or £70,000 for joint (50:50) holders, is not protected.

Some may say, "It can't happen here", but it did in the Isle of Man in 1982, where the Savings & Investment Bank collapsed, losing £42 million of depositors' money. International bank BCCI collapsed in 1991 with debts of £10 billion, hitting 6,500 British depositors - and the legal case against the bank ultimately collapsed as well.

Savings schemes are not safe, either. About £41 million was lost in the Farepak Christmas hamper collapse last year.

The strategy is to know your rights, and to diversify. As Antonio says in The Merchant of Venice:

My ventures are not in one bottom [i.e. ship's keel] trusted,

Nor to one place; nor is my whole estate

Upon the fortune of this present year:

Therefore my merchandise makes me not sad.

Subscribe to:

Posts (Atom)