Adrian Ash in Financial Sense:

BCA Research in Montreal thinks that "sovereign wealth funds" owned by Asian and Arabian governments will control some $13 trillion by 2017 – "an amount equivalent to the current market value of the S&P500 companies."

Monday, November 12, 2007

Sunday, November 11, 2007

Is an irregular cycle a cycle at all?

And 'mid this tumult Kubla heard from far

Ancestral voices prophesying war!

There is a kind of thrill in contemplating destruction - it's a whorl in the grain of human nature. Jeffrey Nyquist indulges this tendency in a piece about Robert Prechter Jnr's views on mass psychology and the markets, and our facing possibly the biggest economic depression since the founding of the American Republic.

You know how everything seems so bright when you get out of the cinema?

Ancestral voices prophesying war!

There is a kind of thrill in contemplating destruction - it's a whorl in the grain of human nature. Jeffrey Nyquist indulges this tendency in a piece about Robert Prechter Jnr's views on mass psychology and the markets, and our facing possibly the biggest economic depression since the founding of the American Republic.

You know how everything seems so bright when you get out of the cinema?

The returning wave

As Japanese currency is getting out of risky investments and heading home, Brady Willett lists the factors putting the dollar under downward pressure:

In recent weeks the markets have speculated that the Saudis may drop their peg, that other Gulf states and sovereign wealth funds in the area are lightening their exposure to the dollar, and that OPEC continues to eye settling in Euros instead of dollars. Also recently China and Japan dumped a combined $33 billion in U.S. Treasuries (in August), and Chinese officials have continued to discuss reducing exposure to the dollar. Suffice to say, that against an already uncertain backdrop U.S. dollar holders are coming forward threatening to fan the flames and talk of the dollar era being over is running hot is hardly encouraging. Less encouraging still is the fact that those who previously cheered the dollar’s decline are turning scared.

He wonders whether we may see an emergency support plan for the dollar.

Saturday, November 10, 2007

Avast behind!

Pearce Financial (Financial Sense, yesterday), like Marc Faber, believes that the East is dangerously overheated and deflation could hit commodities as well as shares; also, the dollar could rise again, and the Japanese yen might break free from its moorings.

I'd like some help with understanding this last, as tides of returning dollars and yen would seem to argue inflation in their home countries.

Karl Denninger (Market Ticker, yesterday) explains it as a relativistic effect:

Our problems are bad. The problems that will be faced overseas are FAR WORSE. Overseas economies are dependant on us, not the other way around. When this sinks in the other currencies against which the DX is measured will collapse; this will appear to raise the dollar, but in fact it is the sinking of other currencies.

"Tom the cabin boy smiled, and said nothing."

Friday, November 09, 2007

Stop engines

Julian Phillips (Financial Sense, today) explains why he thinks central banks may soon have to stop selling gold, and may even need to start buying.

Devil take the hindmost

(Picture source)

(Picture source) The Mogambo Guru vents his muscular spleen on inflation-capping for pensions in Britain. Quite right. The old are spending the kids' inheritance royally. There's so much talk of the selfishness of the young, but the oldies really knock the lights out in that competition.

Red speckles

Paul Nolte (Financial Sense yesterday) strikes a more judicious note. He points out that house price drops do not hit everybody equally, since not everyone has extracted equity and not everyone needs to sell:

... real estate is not like buying 100 shares of Cisco in early 2000 and watching it drop 80% - everyone loses the same amount, very unlike the real estate market. The point – the real estate market is not like the stock market bubble and will take a much longer time to work out – our best guess is an initial bottom is likely in 2009 and we won’t see a meaningful turn higher in overall real estate prices until sometime 2011-2012.

Similarly, there is opportunity for people to cut back on energy consumption in response to higher oil prices.

He expects a bit of a pullback in commodities and precious metals, and currently tends to prefer bonds to stocks.

... real estate is not like buying 100 shares of Cisco in early 2000 and watching it drop 80% - everyone loses the same amount, very unlike the real estate market. The point – the real estate market is not like the stock market bubble and will take a much longer time to work out – our best guess is an initial bottom is likely in 2009 and we won’t see a meaningful turn higher in overall real estate prices until sometime 2011-2012.

Similarly, there is opportunity for people to cut back on energy consumption in response to higher oil prices.

He expects a bit of a pullback in commodities and precious metals, and currently tends to prefer bonds to stocks.

Tough, but believable

Read Karl Denninger's Thursday piece over at Market Ticker. Semi-apocalyptic, but with hopes for America's survival, in what he thinks will be a deflationary depression accompanied by civil unrest and regional conflict in the East.

He thinks it's not too late for the US to recover its economic base. I hope the same for my country.

He thinks it's not too late for the US to recover its economic base. I hope the same for my country.

Thursday, November 08, 2007

Bailing out the gold traders?

Here's an interesting story from Thomas Tan in SafeHaven yesterday:

... There has been a lot of discussion among gold investors on gold manipulation by central banks... I am not quite into the old conspiracy story, but financially I see incentives and benefits for central banks to lease and loan gold to bullion banks during gold's bear market... However if gold is on [an] explosive move like right now, bullion banks will suffer heavy losses when they buy back gold in the open market. Whether this act can be called manipulation and conspiracy? Maybe, but it was probably more financial interest driven, and suppressing gold as secondary goal.

... in May 1999, the then Chancellor Gordon Brown (now Prime Minister) of Britain sold 415 tonnes of gold, almost 60% of its total reserves, leaving Britain with only 300 tonnes. 11 days earlier, Brown had requested the IMF to sell $10 billion of its gold on the open market too. So far no real reason has been officially offered for selling gold in such a hurry... According to Mr. Schoon, it is rumored that British was acting probably in a joined effort with US Fed to save a large Wall St bullion bank which had a 1,000 tonne short gold position loaned by the US government. And it was at the brink of disaster when gold took an unexpected rise at that time in 1999 and the tide was turning against them. If true, this bailout is no different than LTCM and the current subprime bailouts, except the US government had absolutely no choice in this case since it had to rescue the bank and get its gold back.

... No matter what happened then, today it seems: 1) Rise of gold is a nightmare for all CBs since they have been the net sellers; 2) All CBs have less gold than they claim to have, and will run out of ammunition to suppress gold and eventually be defenseless to protect their paper currencies; 3) At the end all CBs will have to turn themselves into net gold buyers from sellers.

... There has been a lot of discussion among gold investors on gold manipulation by central banks... I am not quite into the old conspiracy story, but financially I see incentives and benefits for central banks to lease and loan gold to bullion banks during gold's bear market... However if gold is on [an] explosive move like right now, bullion banks will suffer heavy losses when they buy back gold in the open market. Whether this act can be called manipulation and conspiracy? Maybe, but it was probably more financial interest driven, and suppressing gold as secondary goal.

... in May 1999, the then Chancellor Gordon Brown (now Prime Minister) of Britain sold 415 tonnes of gold, almost 60% of its total reserves, leaving Britain with only 300 tonnes. 11 days earlier, Brown had requested the IMF to sell $10 billion of its gold on the open market too. So far no real reason has been officially offered for selling gold in such a hurry... According to Mr. Schoon, it is rumored that British was acting probably in a joined effort with US Fed to save a large Wall St bullion bank which had a 1,000 tonne short gold position loaned by the US government. And it was at the brink of disaster when gold took an unexpected rise at that time in 1999 and the tide was turning against them. If true, this bailout is no different than LTCM and the current subprime bailouts, except the US government had absolutely no choice in this case since it had to rescue the bank and get its gold back.

... No matter what happened then, today it seems: 1) Rise of gold is a nightmare for all CBs since they have been the net sellers; 2) All CBs have less gold than they claim to have, and will run out of ammunition to suppress gold and eventually be defenseless to protect their paper currencies; 3) At the end all CBs will have to turn themselves into net gold buyers from sellers.

The inflation race

The pound is now worth around $2.10 US, which has some advantages: I know someone who's just had two nice holidays in America this year - to Disneyland and Las Vegas. Anyone who's inclined to sniff should remember that these places, unlike so many in Europe, try really hard to make it fun for you to spend your money.

But why doesn't the pound buy even more dollars? After all, look how gold has soared against the buck. The answer is that most currencies are competing in a devaluation race, as Chris Puplava shows here. The UK is ramping up its money supply at a similar rate to the USA's, but we don't hear so much about it on this side of the water - I think middle-income Americans are generally more clued-up on finance and... is it fair to suggest that they're more patriotic?

For a long time, we've been buying from poor people around the world. They've been storing up the money - you do, when you know how hard you've worked for it and don't want your children to go back to the fields - and now they're not quite so poor. Unemployment is on the rise here, but our trading partners aren't going to pay the Social Security bill for us.

So it's more taxes, or printing more money. The difference between taxation and inflation is the difference between robbery and theft. Theft is less confrontational.

Ron Paul was talking about digital gold currencies five years ago - now watch for the progress of the gold dinar.

But why doesn't the pound buy even more dollars? After all, look how gold has soared against the buck. The answer is that most currencies are competing in a devaluation race, as Chris Puplava shows here. The UK is ramping up its money supply at a similar rate to the USA's, but we don't hear so much about it on this side of the water - I think middle-income Americans are generally more clued-up on finance and... is it fair to suggest that they're more patriotic?

For a long time, we've been buying from poor people around the world. They've been storing up the money - you do, when you know how hard you've worked for it and don't want your children to go back to the fields - and now they're not quite so poor. Unemployment is on the rise here, but our trading partners aren't going to pay the Social Security bill for us.

So it's more taxes, or printing more money. The difference between taxation and inflation is the difference between robbery and theft. Theft is less confrontational.

Ron Paul was talking about digital gold currencies five years ago - now watch for the progress of the gold dinar.

China starts dumping the dollar

Perhaps this is just a little jerk on the chain, to remind us who's on the collar end now.

Financial experts

Commenting on Michael Panzner's scorn for the authoritative pronouncements of some financial experts, I was thinking of a "wizard" story which I've now tracked down. It's been circulating since 1995, but it's worth retelling. Mark Oswald of The New Mexican newspaper reported:

During discussion by the Senate of a serious piece of legislationconcerning the psychology profession last week, Sen. Duncan Scott,R-Albuquerque, proposed an amendment. It says:

"When a psychologist or psychiatrist testifies during a defendant's competency hearing, the psychologist or psychiatrist shall wear a cone-shaped hat that is not less than 2 feet tall. The surface of the hat shall be imprinted with stars and lightning bolts.

"Additionally, a psychologist or psychiatrist shall be required to don a white beard that is not less than 18 inches in length, and shall punctuate crucial elements of his testimony by stabbing the air with a wand. Whenever a psychologist or psychiatrist provides expert testimony regarding the defendant's competency, the bailiff shall contemporaneously dim the courtroom lights and administer two strikes to a Chinese gong."

Usually, anything proposed by Scott - whose hard-core conservatism is like cod liver oil for the Senate's Democratic majority - goes nowhere. But his wizard-hat amendment was warmly received and passed by a voice vote. It is now part of Sen. Richard Romero's psychologist bill, as the measure moves to the House.

Jokes this good usually come with a rider. It was subsequently reported:

The bill, with the wizard amendment, passed the Senate by voice vote and cleared the house by 46-14. Unfortunately, Gov. Gary Johnson vetoed the legislation.

It's extra fun when the authorities play along for a while.

That reminds me... Back in the 1970s, a couple of Oxford undergraduates proposed the building of a full-sized pyramid in one of the University's parks, as a monument to themselves. It went to the University's Hebdomadal Council and the proposal was narrowly defeated (5-4, they say).

During discussion by the Senate of a serious piece of legislationconcerning the psychology profession last week, Sen. Duncan Scott,R-Albuquerque, proposed an amendment. It says:

"When a psychologist or psychiatrist testifies during a defendant's competency hearing, the psychologist or psychiatrist shall wear a cone-shaped hat that is not less than 2 feet tall. The surface of the hat shall be imprinted with stars and lightning bolts.

"Additionally, a psychologist or psychiatrist shall be required to don a white beard that is not less than 18 inches in length, and shall punctuate crucial elements of his testimony by stabbing the air with a wand. Whenever a psychologist or psychiatrist provides expert testimony regarding the defendant's competency, the bailiff shall contemporaneously dim the courtroom lights and administer two strikes to a Chinese gong."

Usually, anything proposed by Scott - whose hard-core conservatism is like cod liver oil for the Senate's Democratic majority - goes nowhere. But his wizard-hat amendment was warmly received and passed by a voice vote. It is now part of Sen. Richard Romero's psychologist bill, as the measure moves to the House.

Jokes this good usually come with a rider. It was subsequently reported:

The bill, with the wizard amendment, passed the Senate by voice vote and cleared the house by 46-14. Unfortunately, Gov. Gary Johnson vetoed the legislation.

It's extra fun when the authorities play along for a while.

That reminds me... Back in the 1970s, a couple of Oxford undergraduates proposed the building of a full-sized pyramid in one of the University's parks, as a monument to themselves. It went to the University's Hebdomadal Council and the proposal was narrowly defeated (5-4, they say).

Wednesday, November 07, 2007

Musical chairs and funny hats

Michael Panzner looks closer to being vindicated as the weeks roll by. Here he quotes Nouriel Roubini on the continuing musical-chairs-type credit tightening - we're getting well beyond sub-prime territory - and castigates the financial astrologers who failed to foretell the oncoming disasters. I think many of them should be made to wear star-bedecked hats, and wave wands.

Down Jones

Dow 9,000 update: Dow at 13,660.94, gold $833.80/oz. "Gold-priced Dow" has therefore gone down since July 6, from 13,611.69 to (effectively) 10,612.71, a drop of 22% (or 52% p.a. annualised).

To put it another way, the Dow has stood still and gold has risen 29% (or 112% p.a. annualised) over the last 123 days.

To put it another way, the Dow has stood still and gold has risen 29% (or 112% p.a. annualised) over the last 123 days.

Tuesday, November 06, 2007

Lenders should tremble

"Genesis" at Market Ticker explains that US lenders who colluded in fraudulent mortgage applications can be forced to have the properties back at their original valuation.

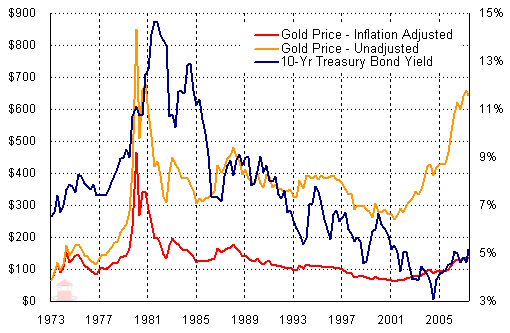

Gold: forget the charts

Gold is currently nearly $820/oz. and it's natural to look at the historical charts to see where this puts us. We did this yesterday.

But what use are the charts? The wiggly lines on them don't show the full context: the wild monetary inflation and cumulative trade and budget deficits of the past few years, which (if we believe the analysts) are unprecedented.

Instead of drawing conclusions from the graphs, we should be asking questions - especially, why hasn't gold zoomed more and earlier? After all, governments must feel that gold is at least a vestigial or potential measure of the worth of their currency; otherwise, they wouldn't be storing thousands of tons of the unproductive stuff in expensive facilities. So, why hasn't gold acted as the thermometer of this financial fever of the last, oh, seven years?

One answer is that the world gold market is small enough to be deliberately distorted. Frank Veneroso could be right: central banks may have been secretly drip-releasing portions of their bullion reserves. That would be to reassure us - or rather, kid us - that everything's under control. Since the gold price matters, it becomes important for officials to manipulate it, and so (according to this theory) the charts will actually tell us nothing.

Until the reserves get so low that the game can't continue. Central banks will suddenly get vertigo and freeze-cling to what they have left, and the gold market will explode, as confidence in the currency starts to collapse.

And Veneroso cottoned on early, simply because the scam worked too well. The smile was too bright, the walk a little too confident. If he's right - and I more than half suspect he is - we needn't bother with the past price data, or with worries about short-term corrections.

But what use are the charts? The wiggly lines on them don't show the full context: the wild monetary inflation and cumulative trade and budget deficits of the past few years, which (if we believe the analysts) are unprecedented.

Instead of drawing conclusions from the graphs, we should be asking questions - especially, why hasn't gold zoomed more and earlier? After all, governments must feel that gold is at least a vestigial or potential measure of the worth of their currency; otherwise, they wouldn't be storing thousands of tons of the unproductive stuff in expensive facilities. So, why hasn't gold acted as the thermometer of this financial fever of the last, oh, seven years?

One answer is that the world gold market is small enough to be deliberately distorted. Frank Veneroso could be right: central banks may have been secretly drip-releasing portions of their bullion reserves. That would be to reassure us - or rather, kid us - that everything's under control. Since the gold price matters, it becomes important for officials to manipulate it, and so (according to this theory) the charts will actually tell us nothing.

Until the reserves get so low that the game can't continue. Central banks will suddenly get vertigo and freeze-cling to what they have left, and the gold market will explode, as confidence in the currency starts to collapse.

And Veneroso cottoned on early, simply because the scam worked too well. The smile was too bright, the walk a little too confident. If he's right - and I more than half suspect he is - we needn't bother with the past price data, or with worries about short-term corrections.

Monday, November 05, 2007

Start like Buffett to end up like Buffett

Great article in The Motley Fool about how Warren Buffett founded and developed his fortune, and some of us could do the same.

Gold: undervalued, or not?

Boris Sobolev (SafeHaven, today) reckons gold is still well below its inflation-adjusted high of $3,000. But the chart he refers us to from his previous article (Resource Stock Guide, June 8) could be interpreted as showing that gold (in real terms) is now around its long-term trend. In that case, surely only a speculator would hope for a new spike to make a quick killing.

Warren Buffett and derivatives

John Carney, in DealBreaker.com today, discusses Warren Buffett's recent involvement in derivatives, notwithstanding his previous publicly-announced disenchantment with the product. Does he understand the risks better this time around, or has he simply worded the contracts more carefully?

Sunday, November 04, 2007

The Inflation Protection Quandary

A succinct article by Weamein Yee in Banks.com (Friday), on what to do in inflationary times:

It’s almost like everyone is holding their breath to see what happens next.

As we know, Marc Faber recently suggested we might wish to stand on the platform rather than board any of the asset trains.

Stocks will tend to fall in anticipation of higher interest rates to combat rising inflation. The price of long term bonds will fall as investors will demand higher yields in an inflationary environment.

Yee says that the investor may be forced to consider choices that would normally be regarded as rather risky or sophisticated: commodities, precious metals and shares in foreign (less inflation-prone) countries. This is the paradox: taking a risk may be the best form of playing safe.

But before that, perhaps we could increase our holdings of government-backed inflation-linked savings bonds, something Yee doesn't mention. A lot depends on how the government defines inflation for the purpose of calculating our returns, but it should be fairly reasonable, one would hope.

The writer points out a final irony: low interest rates and high inflation support real estate prices.

It’s almost like everyone is holding their breath to see what happens next.

As we know, Marc Faber recently suggested we might wish to stand on the platform rather than board any of the asset trains.

Stocks will tend to fall in anticipation of higher interest rates to combat rising inflation. The price of long term bonds will fall as investors will demand higher yields in an inflationary environment.

Yee says that the investor may be forced to consider choices that would normally be regarded as rather risky or sophisticated: commodities, precious metals and shares in foreign (less inflation-prone) countries. This is the paradox: taking a risk may be the best form of playing safe.

But before that, perhaps we could increase our holdings of government-backed inflation-linked savings bonds, something Yee doesn't mention. A lot depends on how the government defines inflation for the purpose of calculating our returns, but it should be fairly reasonable, one would hope.

The writer points out a final irony: low interest rates and high inflation support real estate prices.

Subscribe to:

Posts (Atom)