Wikipedia estimates the world's stockmarket capitalisation at $51 trillion and bonds at $45 trillion. Taken together, in sterling terms, that's about £49 trillion. So in seven years' time, sovereign funds are expected to control 12% of the market. This is significant: you'll recall that and EU countries require declarations of shareholdings at various levels between 2 and 5 per cent (3% in the UK), as seen in Appendix 5 of this document, and anyone owning over 1% of a company's shares has to declare dealings if the company is the subject of a takeover bid.

My hazy understanding of democracy is that it includes two crucial elements, namely, the vote, and the right to own personal property. We're losing both. What is our freedom worth when collectively, governments not only employ large numbers of people directly, but many more of them indirectly, through ownership of the businesses for which they work?

What does the vote matter? Here in the UK, we have had a coup by a small, tightly organised (and unscrupulous, even if and when principled) group who have realised that what matters is the swing voter in the swing seat, and nothing else. "What works is what matters" - a slogan that, superficially, seems simply pragmatic, but actually slithers away from identifying the principal objective: you can only tell if it works, when you know what you want it to do. And under our first-past-the-post system, with constituencies determined (how? and who is on the committee?) by the Boundary Commission, I could vote for the incumbent or the man in the moon, but I'm going to get a Labour Party apparatchik in my ward.

And I don't think the system will be reformed if "the other lot" get in, either: "Look with thine ears: See how yond Justice rails upon yond simple thief. Hark in thine ear: Change places, and handy-dandy, which is the Justice, which is the thief?" Structural issues matter: we are cursed by the psephologists, spin doctors and databases.

And as for property, when sovereign wealth funds go from being the tail that wags the dog, to becoming the dog, multinational businesses will be less concerned to satisfy the local shareholder, who may also be an employee. Big MD (or Big CEO) will have his arm around the shoulders of Big Brother.

We worry so much about wealth, and forget what it's for: not just survival, but independence, respect, liberty. Now, the peasants are fed, housed, medically treated, given pocket money, have their disabilities catered for, their children taught, and their legal cases expensively considered. So many of them are fat, enforcedly idle, addled with drink and drugs, chronically ill and disabled, negligent of their offspring and familiar to the point of contempt with the legal system. Despite (because of) their luxuries, they suffer, like the declawed, housebound cats in some American dwellings.

What matters is what works; these outcomes don't matter, except that they work for a class - which I think is becoming hereditary - that seeks, retains and services power. I have said to friends many times that we are seeing the reconstruction of a pan-European aristocracy, disguised as a political, managerial and media nexus.

The American Revolution was about liberty, not wealth, and it is one of the few major nations where the mice did, for a long time, succeed in belling the cat; there was a period here, too, when Parliament could call the King's men to a rigorous account. Now, even in America, the abstract networks of money and power are turning the voters into vassals of the machine that sustains them. As here, the political issues there will soon be welfare, pensions, Medicare and other elements of the badly-made pottage for which we sell our birthright.

As for Bombardier Yossarian in Catch-22, the first step back to our liberty is to stop believing in the benevolence of the system.

BTW: the man who wrote "The Anarchist Cookbook" later converted to Christianity. The one thing not to do with the system is to try to smash it - you'll only get something worse.

... and here's another from

... and here's another from

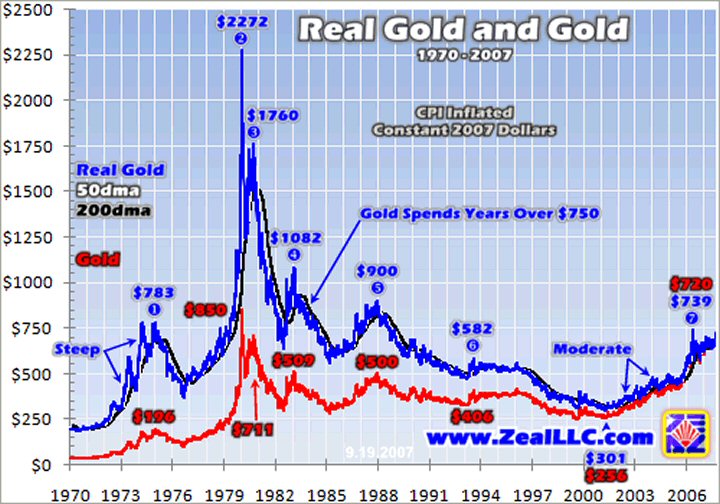

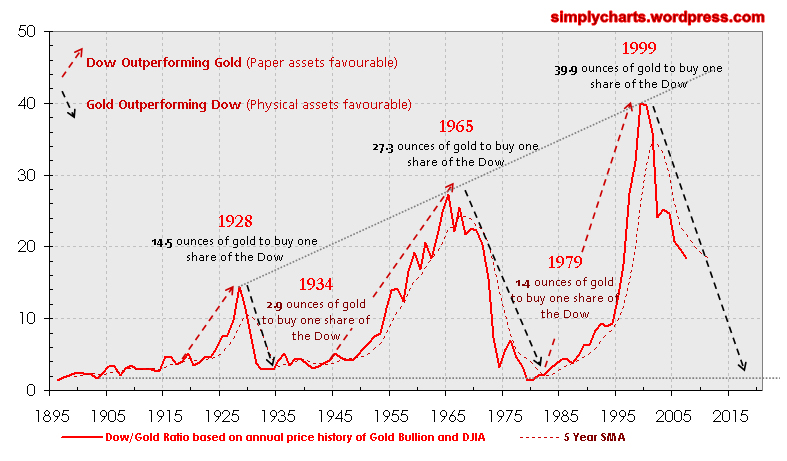

It seems harder to spot an average here, since each peak is much higher than the one before. But taking the Dow as it is now (12,606.30) and the current price of gold ($894.90), the present ratio of 14.08 ounces would be in the middle range of the variation since the mid-1920s.

It seems harder to spot an average here, since each peak is much higher than the one before. But taking the Dow as it is now (12,606.30) and the current price of gold ($894.90), the present ratio of 14.08 ounces would be in the middle range of the variation since the mid-1920s.

{kind=link}