I'm still convinced that many in the financial community deserve far harsher treatment than they've so far received - if they didn't know what would happen, they should have.

But I've been casting about for some deeper structural reason - what allowed financiers to kid themselves that they were acting reasonably, or at least assure themselves that they had followed official guidelines and were "covered"?

So I looked for something relating to the regulation of fractional reserves, and came across references to the Basel Accords (I and II). These are an attempt to "harmonise" central banking policies in developed nations, and perhaps can serve as an object lesson (especially for EU enthusiasts) about international legislation.

Here is the conclusion of an analysis of the two Accords (highlights mine):

One very important fact to assess is the achievements and limitations of each Basel Accord. The first Basel Accord, Basel I, was a groundbreaking accord in its time, and did much to promote regulatory harmony and the growth of international banking across the borders of the G-10 and the world alike. On the other hand, its limited scope and rather general language gives banks excessive leeway in their interpretation of its rules, and, in the end, allows financial institutions to take improper risks and hold unduly low capital reserves.

Basel II, on the other hand, seeks to extend the breadth and precision of Basel I, bringing in factors such as market and operational risk, market-based discipline and surveillance, and regulatory mandates. On the other hand, in the words of Evan Hawke, the U.S. Comptroller of the Currency under George W. Bush, Basel II is “complex beyond reason” (Jones, 37), extending to nearly four hundred pages without indices, and, in total, encompassing nearly one thousand pages of regulation.

The author's concern is that the rules can permit the risk of assets in emerging markets to be understated, and as it turns out the Trojan horse came in through another gate; but in complexity lies opportunity, and in rule-following lies the illusion that personal responsibility is thereby written off.

Showing posts with label Basel Accords. Show all posts

Showing posts with label Basel Accords. Show all posts

Tuesday, December 02, 2008

Sunday, November 23, 2008

Bank crashes and the Basel Accords

I need information and understanding - please help me, somebody.

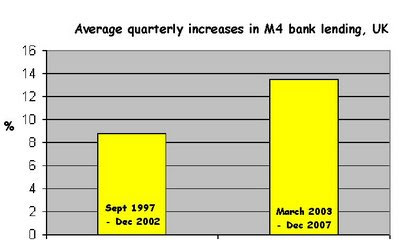

I've pointed out more than once that M4 bank lending in the UK accelerated from 2003 on, and I suspected it was something to do with reducing bank capital adequacy requirements, so the government (via its regulators) would have been implicated. In other words, I've been looking for the villain of the piece, and the smoking gun.

But do you think I can find them?

What I have found so far is references to the Basel Accords, Basel I and Basel II. Basel I became law in the G10 countries including the UK in 1992, and Basel II was published in 2004. The general drift, I understand, is to encourage a uniformity of approach to systemic financial risk, and to introduce a system of risk-weighting bank capital according to what the banks are lending against or investing in. What a success that has proved! Perhaps we should refer to the scheme as "Basel Fawlty".

But can somebody help unpack and simplify what actually happened? Is it, for example, possible that this system was perceived by the banks as a more pliable alternative to fixed minimum reserve ratios, and so they reduced the cash in their vaults to the very least that they could tweak the definitions? For example, we have read many times how mortgage-backed securities are at the heart of the subprime problem, because the packages could be represented as having much less risk than they actually contained.

So is the present crisis an unintended consequence of more elastic international regulation, dating back as far as the early 1990s?

Subscribe to:

Posts (Atom)